POLICIES AND PROCEDURES

|

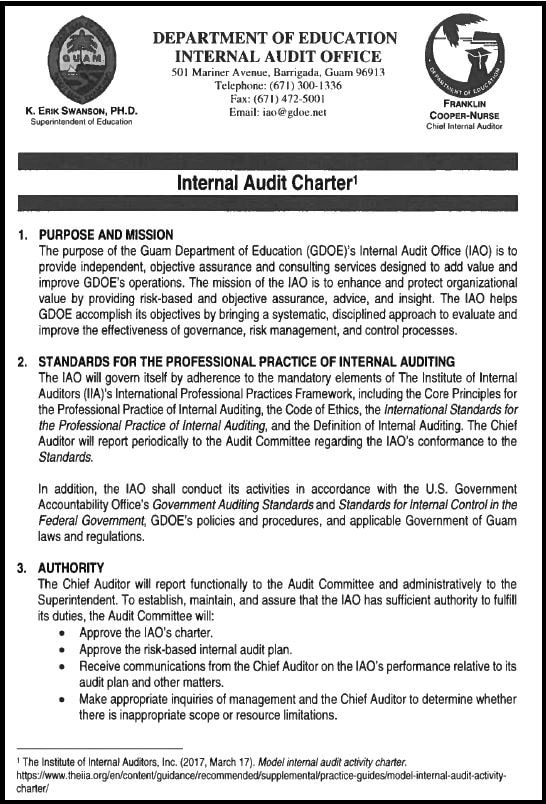

Internal audit charterThe Internal Audit Charter is a formal document that defines the internal audit activity's purpose, authority, and responsibility. The charter establishes the internal audit activity's position within the organization, including the nature of the Chief Internal Auditor's functional reporting relationship with the board; authorizes access to records, personnel, and physical properties relevant to the performance of engagements; and defines the scope of internal audit activities. Final approval of the internal audit charter resides with the Guam Education Board Audit Committee.

|

|

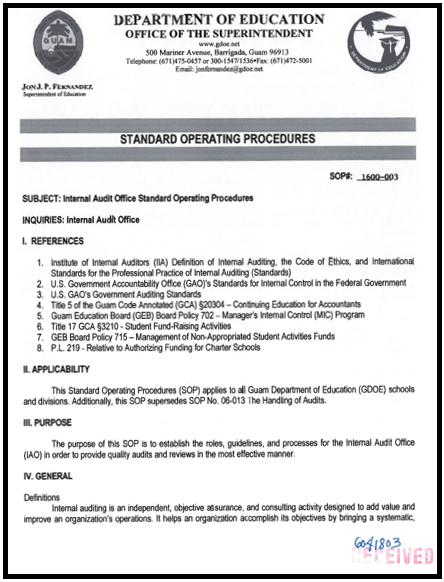

internal audit sop 1600-003In April 2016, Internal Audit Office (IAO) Standard Operating Procedures (SOP) 1600-003 was approved. The SOP established roles, guidelines, and processes for the IAO in order to provide quality audits and reviews in the most effective manner. Under the Superintendent's direction, the IAO has the authority to conduct any audits, reviews, and special requests or investigate any matters within its scope of responsibilities with or without notice to management and/or external parties.

In conducting its audits, the IAO audit staff is required to abide by the Institute of Internal Auditors' Definition of Internal Auditing, the Code of Ethics, and the International Standards for the Professional Practice of Internal Auditing; and U.S. Government Accountability Office’s Standards for Internal Control in the Federal Government and Government Auditing Standards. |

|

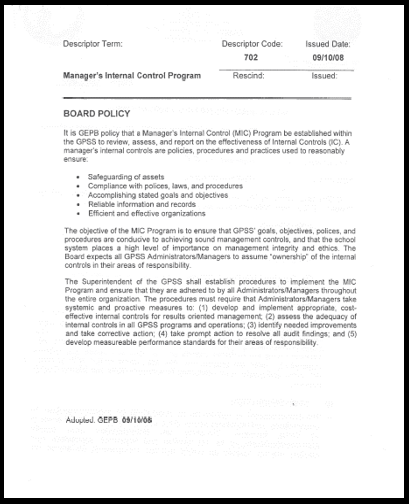

board policy 702In September 2008, Board Policy 702 established the Manager's Internal Control (MIC) Program. In January and May 2009, the Guam Department of Education (GDOE) reported to the U.S. Department of Education (ED), in its Comprehensive Corrective Action Plan, that a new MIC Program has been implemented. ED viewed the MIC Program as a major component for educating and emphasizing the need for the GDOE to embrace such a program.

In May 2014, the MIC Program was strongly implemented. The IAO required for all division heads, school principals, and management to complete the MIC Assessment. Overall, the MIC Program details internal control standards that ensure the operation of internal controls over financial reporting and provides for the prevention or detection of financial misstatements on a timely basis and ensure GDOE's ability to initiate, authorize, record, process, and report financial data consistently and reliably. |

|

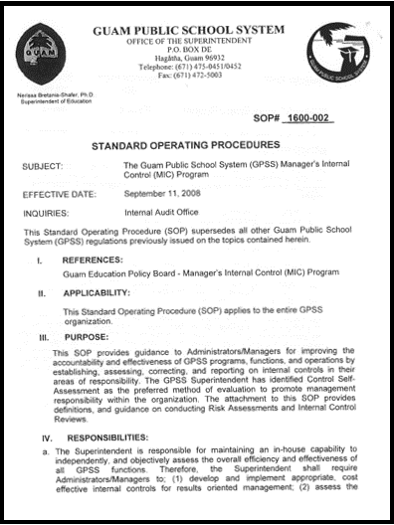

mic sop 1600-002Effectuated in September 2008, the MIC SOP 1600-002 delineates the applicability, purpose, responsibilities, and procedures of the MIC Assessment Program. In accordance with MIC SOP 1600-002, the IAO is to complete an analysis of the MIC assessments.

The MIC Assessment is a self-assessment tool used by the GDOE which provides a good starting point for identifying high risk areas within GDOE schools and divisions. Its objective is to ensure that GDOE's goals, objectives, policies, and procedures are conducive to achieving sound management controls and emphasize the importance of management integrity and ethics. The MIC Assessment allows the responder (or participant) to evaluate three areas of his/her division or school's program or administrative function's management control system: (1) General control environment, (2) Inherent risk, and (3) Safeguards. |

board policy 715 |

|

Issued in August 2005, Board Policy 715 Management of Non-Appropriated Student Activities Funds, specifies two types of Non-Appropriated Fund (NAF): Student Activity Funds (SAF) and Campus Activity Funds or Trust and Agency Fund (TAF). SAF are cash raised, with the GEB’s approval, by students for student organization activities. TAF are cash proceeds from activities such as the DEED program, rent, lab, parking, food contractors, wet garbage, and donations. SAF and TAF are Agency Funds held in trust by the school for the benefit of the student organization, of the whole student body.

|

|

naf sopEach school shall have SOP's to properly account for Non-Appropriated Fund (NAF) receipts and disbursements and the IAO shall audit each school activities fund as often as required, but at least annually. The NAF SOP applies to all GDOE personnel participating in the Student Activity Process. NAF are specified by Guam Education Board Policy 715 and enabled by Public Law 26-26.

|

|

Technical Assistance program grant sop 1600-004In July 2019, the Technical Assistance Program (TAP) Grant SOP 1600-004 was established to prescribe the roles, guidelines, and processes for the TAP grant awarded to the IAO. The TAP grant was awarded to the IAO for a training program to develop and enhance skills and knowledge of audit (compliance monitoring) and accounting personnel from the IAO and GDOE Financial Affairs.

|

|

hotline sop 1600-005In November 2015, the IAO launched its Fraud Hotline. The purpose of the hotline is to establish a means for government employees, the general public, or vendors to file a complaint, concern, or to report suspected waste, fraud, or violations of GDOE policy by any individual working for or doing business with GDOE.

In March 2020, the Hotline SOP 1600-005 established the roles, guidelines, and procedures for the receipt, retention, review and investigation of complaints and citizen concerns reported directly to the GDOE IAO Hotline. The GDOE Superintendent and the IAO encourage any concerned individual to report financial fraud, waste, or abuse involving a GDOE employee or vendor. |

|

Payroll reimbursement validation SOp 1600-006In November 2020, the Payroll Reimbursement Validation SOP 1600-006 established the roles, guidelines, and procedures for the IAO's monitoring, validation, and reporting of payroll reimbursements for the GDOE.

|

accessibility notice

Contact [email protected] to request access to or notify GDOE about on-line information or functionality that is currently inaccessible. For information about how to file a formal grievance with GDOE under section 504 of the Rehabilitation Act of 1973 and Title II of the American with Disabilities Act of 1990, please see GDOE's grievance procedure at https://sites.google.com/a/gdoe.net/gdoe/accessibility-grievance-procedure.