{kind=link}

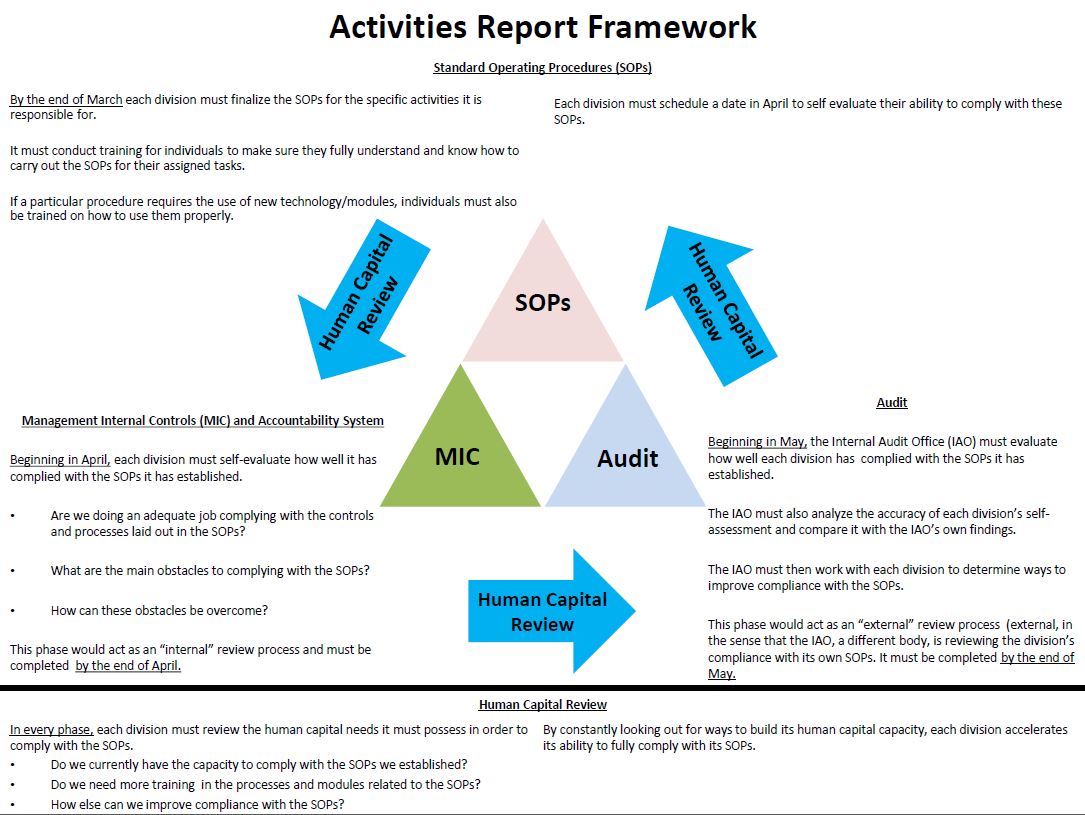

The Department identified 21 critical SOPs for the financial management transition of Third Party Fiduciary Agent (TPFA) activities back to the GDOE. In light of ED's 2016 Special Conditions, GDOE management agreed to provide ongoing training on SOPs to employees requiring them to understand, certify, and comply with the SOPs. Moreover, based on the September 2016 Comprehensive Corrective Action Plan (CCAP), updates and training sessions, finalization of updated SOPs were scheduled to be substantially completed by the end 2016. As per the CCAP, IAO is to conduct tests of internal controls to verify compliance to procedures stated in the approved SOPs. SOP compliance testing was initiated as part of IAO’s 2015-2017 Audit Plan to address special condition requirements for the completion and testing of all SOPs listed in GDOE’s Transition Plan. Upon full implementation of the CCAP, Transition Plan, and testing of critical SOPs identified, the GDOE will commence its formal request to the ED for the reconsideration of special conditions imposed on the Department.

IAO Report no. 19-10

|

[CURRENTLY IN PROGRESS]

The review of GDOE SOPs 200-020 and 200-025 was engaged on October 31, 2018 and is part of IAO's 2018-2020 Audit Plan. The scope of the review will be from October 1, 2016 to September 30, 2018 (or fiscal years [FY] 2017 to 2018). |

IAO REPORT NO. 19-08

|

Financial Affairs was overall partially compliant to SOP 200-017 and related SOPs 200-022 for bank reconciliation and 200-034 for cash disbursements. Specifically:

|

iao report no. 19-07

|

[CURRENTLY IN PROGRESS]

The review of GDOE SOPs 200-026 and 200-027 was engaged on March 8, 2019 and is part of IAO's 2018-2020 Audit Plan. The scope of the review will be from October 1, 2017 to September 30, 2018 (or FY 2018). |

IAO REPORT NO. 19-06

|

GDOE's Supply Management Office (SMO) was overall compliant to SOP 200-033 and overall partially compliant to SOP 200-031. Deficiencies found were:

|

IAO REPORT NO. 19-05

|

The use of emergency procurement is better aligned to laws and procedures which require the existence of emergency conditions. Whereas, past audit reviews disclosed emergency procurement was used frivolously and emergency conditions were a result of poor oversight. During FY 2017 and FY 2018, SMO did not conduct any emergency procurement. SOP 200-030 is also sufficient to ensure compliance to applicable laws and regulation. Therefore, there are no files that warrant further review with regards to SMO’s compliance to the SOP.

|

IAO Report NO. 19-01

|

Financial Affairs was overall non-compliant based on three major components of SOP 200-039. Specifically:

|

time and effort certification

|

An audit of time and effort certification and time distribution was included in IAO's 2015-17 Risk Based Audit Plan due to the level of inherent risk. Additionally, the testing of SOPs by the IAO is a requirement stated in the FFY 2017 Special Conditions Letter. In December 2016, the audit was suspended until the formal adoption of the revised SOP.

In January 2019, ED issued its Final Reconsideration Evaluation Plan requiring the IAO to provide a random sample of assessments of overall progress to be submitted to ED on July 2019. As such, the IAO will re-engage its time and effort review on May 2019. |

IAO REPORT NO. 18-03

|

Based on our limited scope review, we determined Business Office to be in general compliance to SOP 200-044 Reporting of Federal Grant Awards - Schedule of Expenditures of Federal Awards (SEFA) and SEFRAD. However, we observed deficiencies with cash receipts not derived from Munis General Ledger cash account; incomplete project numbers in the SEFRAD; lack of evidence for timely approval of monthly SEFA and SEFRAD reports; and untimely training on SOP 200-044. The SOP adequately established workflow for SEFA and SEFRAD; but, did not provide details to trace the amounts in the SEFRAD. Though deficiencies were identified, the SEFA and SEFRAD are reliable reports of federal grants/assistance revenues and expenditures.

|

IAO report No. 18-01

|

Our limited review revealed that SMO partially complied with SOP 200-018 (original [dated September 2014] and amended [dated August 2016]) on Sole Source procurement. Specifically, we found deficiencies related to insufficient documentation for Sole Source justification (i.e., Determination of Need, and Internal Memorandum from the End User and/or End User Memorandum), and lack of additional supporting documentation for certain transactions. Moreover, we noted additional areas of improvement for management’s consideration related to the enhancement and completeness of SOP 200-018.

|

Iao report no. 17-03

|

SOP 200-041, effective in October 2015, was adequately designed to establish policy and procedures for administering school meals and cash collections. Based on our limited scope review, we determined partial compliance to the SOP. Areas of non-compliance include (1) practices not aligned with policy; (2) differences in the schools' School Meals Collection Report of ($121) and Monthly Meal Count Report of (21); (3) differences of $1,212 and incomplete attachments in Munis; and (4) no training on the SOP. We also noted the need to improve its sections on Procedures, Internal Control, and References sections. Further, the SOP should be amended to address overlapping procedures form SOP 600-001 for IOUs and SOP 200-012 for bank deposits.

|

iao report no. 17-02

|

An audit of fixed assets was included in IAO's 2015-17 Risk Based Audit Plan due to the level of inherent risk. Additionally, the testing of SOPs by the IAO is a requirement stated in the U.S. Department of Education FFY 2016 Special Conditions Letter. IAO completed an audit of SOP 200-015 Fixed Asset Management for Property Management Office (PMO) and Central Receiving Warehouse, and SOP 200-019 Fixed Asset Management for School's and Divisions.

Based on IAO's review, we identified deficiencies in three major component areas comprised of purchasing and receiving, recording and tracking (i.e., asset identification, recording of asset information, and asset location responsibility), and classification of asset disposition (i.e., survey of assets, lost/stolen assets, and asset recovery). To improve accountability, we recommended (1) PMO exercise increased oversight and coordination over the receiving of assets. Receiving documents should be maintained electronically; (2) Strengthen processes related to missing asset tags to include; (3) PMO decrease frequency of annual inventory inspections for the locations that received good performance ratings; (4) PMO coordinate with TPFA to establish new guidelines for consideration of increasing fixed assets dollar threshold, going from $500 to $5K, in accordance with federal guidelines; and (5) PMO enhance guidelines on imposing appropriate sanctions for the monetary recovery of assets and apply the appropriate depreciation calculation for remittances. Overall, GDOE's administration over fixed assets was deemed as “General Compliance.” |

IAO Report no. 16-02

|

In response to a citizen concern reported to GDOE, IAO completed an audit of the administration of off-island travel relating to the 2015 International Society for Technology in Education and National Center for Education Statistics Data conferences.

Our audit revealed deficiencies surrounding off-Island travel procedures, questionable travel management practices, and the prudent use of federal funds. As a result, questioned costs amounted to $2,090 and we identified missed opportunity for cost savings totaling $31,008. |

ACCESSIBILITY NOTICE

Contact [email protected] to request access to or notify GDOE about on-line information or functionality that is currently inaccessible. For information about how to file a formal grievance with GDOE under section 504 of the Rehabilitation Act of 1973 and Title II of the American with Disabilities Act of 1990, please see GDOE's grievance procedure at https://sites.google.com/a/gdoe.net/gdoe/accessibility-grievance-procedure.